It had to happen. I was miserable. I knew it was time to move on.

But, that’s not all.

It cost me $1,000,000 to do it.

Hold on a sec. Let’s rewind.

In our last article, we examined the case study of PhysicianOnFire and how he will retire by 45.

However, for many of us, that simply isn’t a reality. Retiring by 45? You might think this is impossible. You might even think that is crazy. Maybe you are looking at retiring at 50, 55, 60, 65, or even 70 years old.

Maybe that’s frightening and scary for you. Guess what? You’re not alone. I’m there too. I can’t retire by 45. It’ll probably be 60 or 65.

Let me explain more.

You see, what happened was over a decade ago I was an employee. As a matter of fact, I was the best employee my boss ever had. That’s his words by the way, not mine.

I was compensated handsomely, but it wasn’t enough for me. I wanted control over my destiny.

It was 2008. My boss was going through a nasty divorce and he wasn’t present. The financial crisis was around the corner, but who knew?

I was 27 years old and I was ready to take a risk.

Before we go much further, I have a confession to make. I have to be honest, it’s really hard to bare my soul.

I’m about to share something with you that is painful and even embarrassing.

However, I feel I need to be transparent with you.

I hate debt with a passion. And that’s because… it’s personal.

Like many physicians, my family and I have been working our way out of hundreds of thousands of dollars of debt.

In my case, it wasn’t for education. That was paid off years and years ago.

At the time, it wasn’t for a house. As a matter of fact, our mortgage was completely paid off.

It wasn’t even for a car loan or for some fat hedonistic pleasure. We’ve always paid for our cars in cash and kept our living expenses modest.

My debt in multiple six figures was to acquire a practice.

Back on August 1st, 2008, my wife and I took a huge leap of faith and made a $1 million acquisition.

Great timing, right?

Let’s just say that we went through some very excruciating times in the first years.

Why the heck did we make the acquisition?

At the time, I was ready to break-free from my situation. I was stuck on “assembly-line finance” and was getting more and more frustrated.

I was sick & tired of being an employee making money for someone else & not reaping much of the reward.

I had in my heart that I wanted to run the show, that I wanted to control my own destiny. As a matter of fact, I felt a bigger calling in my life.

However, at the same time, I wanted to maintain my standard of living. I didn’t want to start from scratch.

So, we dove headfirst into this financial quagmire.

Luckily, we had plenty of money in the bank, and put down more than 30% as a down payment.

We leveraged our house that previously had NO debt. On top of that, we sucked all of the money out of savings- which was over six figures at the time.

It was kind of like the Titanic. We go big or we go-home. I was on front of that big old ship screaming out that I was “King of the World.”

We were all-in on this deal. The stars were shining in my eyes. Hollywood-or-bust!

With the rest of the funds, I borrowed money from family.

That’s right- multiple six figures in family loans. Luckily, I was blessed in that sense- it wasn’t money from the bank.

When things didn’t turn out like I hoped, at least family could be understanding and was much easier to work with.

However, on the other hand, as we’ve made headway- paying back hundreds of thousands over the last 8 years- there’s this feeling of guilt. I should have paid them off years ago. This is my family! They’ve helped me out, They deserve their hard-earned money back.

That’s why you are reading and hearing my passion about the importance of eliminating debt throughout the years. Needless to say, it’s been a personal struggle & I’ve learned plenty of lessons along the way.

Anyhow, needless to say this huge transition drastically effected my ability to retire early. However, in my case, I never planned on retiring early anyhow.

The great news is that this acquisition involved building equity. It’s kind of like buying a house. You give up a whole bunch of cash in order to build more equity for the future to ensure that you are not paying rent.

I have over $500,000 of equity in my business. So, we have a very real asset that has grown in value since we started, despite a rocky start.

If I wanted to step away from the business, I certainly could and walk away with substantial cash in the bank.

Yet, there’s really more to this story. There are several reasons why I won’t retire early. Discover them below…

5 Reasons Why I Won’t Retire Early

Reason# 1: I Don’t Have An Employer With Benefits

The cruddy thing about being self-employed is that the only benefits I have are the ones I give to myself.

There’s no company 401k match unless I use my own company dollars.

There’s no company healthcare plan.

There’s no pension or other perk.

Of course, don’t get me wrong… there’s all sorts of fantastic tax write-offs and I can allocate my hard-earned money how I want.

However, this does make the day-to-day life much more expensive.

Need braces? It’s out of pocket.

Trip to the E.R.? It’s out of pocket unless we go a whole bunch and the max deductible is met.

This means I have a lot less security and I have to keep working well past 50 in order to earn enough to meet all of those needs as both employer and employee.

I feel kind of like Spidey when his spidey sense is tingling. I’m always on the look-out and ready to jump at any moment.

Reason# 2: We Are (Currently) A Sole-Bread Winning Family

Once we moved to Minnesota in 2008, my wife aspired to many different dreams. She’s an amazing lady and she is super driven.

We purposely chose to have her stay at home for a time. Sure, she’s worked a few odd jobs here and there. She worked at Children’s Place for a year or two. She worked at Kohl’s for a year or two. She worked at our church directing praise and worship for a couple of years.

None of those were more than 20 hours a week and none of those have benefits.

Also, we got hit with the joy and challenge of our 12.4 ounce daughter. That’s slowed us down some.

However, that was 4.5+ years ago now.

With our youngest miracle kiddo going to kindergarten this fall, there’s a possibility my wife could have the bandwidth to do a longer-term commitment.

However, my wife doesn’t want that kind of gig. She’d probably hate that. Because I’m an amazing, loving, and supportive (sometimes) hubby, I’m cool with her doing her thing.

She’s now starting her own podcast and has a band. You can check them out at www.seedbandofficial.com.

Also, a wise man once told me that a happy wife is a happy life.

Unfortunately, that happiness means that we have less income currently coming in that we could if both of us were working.

This of course means that we can’t save as much and retirement will be delayed unless my practice or her band or both brings in a bunch of unexpected dough and blows up.

Reason# 3: We Were Raised Differently In Thinking About Money

My family and I are pretty frugal about many things, but perhaps not as much as our friend PhysicianOnFire.

My folks and grandparents were definitely into pinching pennies. The principle of saving was right next to the golden rule.

We had to save, save, and save some more.

Don’t get me wrong. My folks have our foibles. However, my mom and dad weren’t averse to going to Goodwill or doing some of the little things that drive my wife nuts.

One of the habits that she pokes at me with verbally is the habit of reusing Ziploc baggies. You see- if Ziploc baggies have had veggies, fruit, or chips or something like that- I will wash those baggies and reuse them.

She claims that this is ‘ghetto’. Then, she promptly throws them out before they properly dry and I stand there shaking my head.

I mumble under my breath, “Every penny counts!” She retorts back, “Whatever! That’s so ghetto! Where did that come from?”

Then, she laughs at me mercilessly and throws away another one while I stand their dumbfounded shaking my head.

Yet, this little microcosm shows us an important lesson.

We were raised differently to think about resources and money.

I’ve rubbed off on her and she’s rubbed off on me.

I’m not as penny pinching as I used to be. (Most of) my clothes don’t have holes in them anymore. They are newer and shinier. She is more penny penching and budget conscious than she used to be.

We still don’t have any car loans and have a very comfortable amount in the bank and in our brokerage accounts.

Over the last 14 or so years or marriage, I’ve found that staying married is a hell of a lot cheaper than getting a divorce… even if I rewashed and reused my Ziploc baggies.

Reason# 4: We Give A Lot Away

In a future blog post, I am going to take more about the role of faith & finances for my family.

To make a long story short, we are dedicated to giving. We give about 10% of income to our church. This is at least low five figures every single year.

In addition, we want to sew into the lives of the next generation. We give a small scholarship every single year to the business school at our alma mater, Seattle Pacific University.

Giving is a very important part of our journey and it may well delay our retirement by over a decade because otherwise we could have banked that 10% in our retirement and brokerage accounts.

Reason# 5: I Like My Job (Most of The Time)

Many physicians are struggling with burnout. I have too from time to time.

Luckily, I’m blessed with being able to set my own schedule. So, if I really need to take time off I can.

Thus, being in control gives me a high degree of freedom. I can work as hard (or as little as I want).

I can keep doing this for a very, very long time. If everything falls apart, I am confident that I could make a fantastic salary elsewhere and the family will be fine.

The Healthy Financial Habits My Family Has Developed

I have to confess…. maybe we aren’t as prosperous financially as we could be.

However, I am really proud of some specific habits we developed that will lead to us retiring down the road securely.

Here are some of the great financial habits that help us and maybe will help you too:

- We pay for every big ticket item in cash. We bought our last ‘new to us’ vehicle in cash and we are saving up to do so again.

- We have no extra big boy toys or expensive hobbies. No skimobiles. No jet skis. No boats. No golfing. No skiing.

- We have a grocery/eating out budget to track to the penny what we spend every month. Frankly, this can back fire from time-to-time. My wife gave me the death stare when we went to Costco the other day when I was adding up each item to keep us under $200 when we went grocery shopping. I kept saying… no, no, and no. How about this or that? Let’s just say that she doesn’t enjoy shopping with me.

- We have a very minimal mortgage which gives us flexibility. It’s only about $950/month and if we wanted to devote resources there, we could pay it off in a decent time.

- We fly sometimes to save time to see family across the country, but other times we save money by taking a road trip. Buying 4 plane tickets each way gets expensive!

- We have no loyalty to any company and find the cheapest deal for travel when we do fly. Those extra perks and rewards for airline travel often add up astronomically.

- We never fly first class or pay extra for leg room

- We stay with family when we travel together rather than renting a house or a hotel

- We save systematically every single month into brokerage accounts and lump sum extra amounts of cash to pay off debt

- Our kids go to fantastic public schools which avoids having to pay extra for private school

- When we go on dates, most of the time we use credit card rewards so that the only cost is baby sitting

- We live in the Midwest where it is pretty cheap & reasonable relative to the cost of living on the coasts

- We invest in our marriage by going on dates at least once a month and a one or two day getaway 2x a year

I don’t write this to give myself a pat on the back. Well… maybe I am. But we have our guilty pleasures too.

- We have regular old expensive cable through Comcast and haven’t cut the cord yet

- We have regular expensive cell service through TMobile

- We are into the trendy and sometimes expensive gluten-free diet. We’re buying gluten free this and that. If it’s gluten free, it’s healthy right?

- We like going to movies and buying popcorn (but not soda). Although, again we use credit card rewards here.

- We have a timeshare which we’ve loved using for seeing all parts of the country. It’s not really a huge money suck. Although, it’s not a great financial investment either since it is a liability rather than an asset. All that being said, we bought it in cash and never had debt on it. We’ve had many, many great family moments at the places we stayed which we would never have otherwise been to. I’m good with that even if it isn’t the most efficient use of our money.

How I Can Afford To Retire (But Not at 45)

Are you ready to nerd out?

Let’s crunch some numbers to see how my retirement could work!

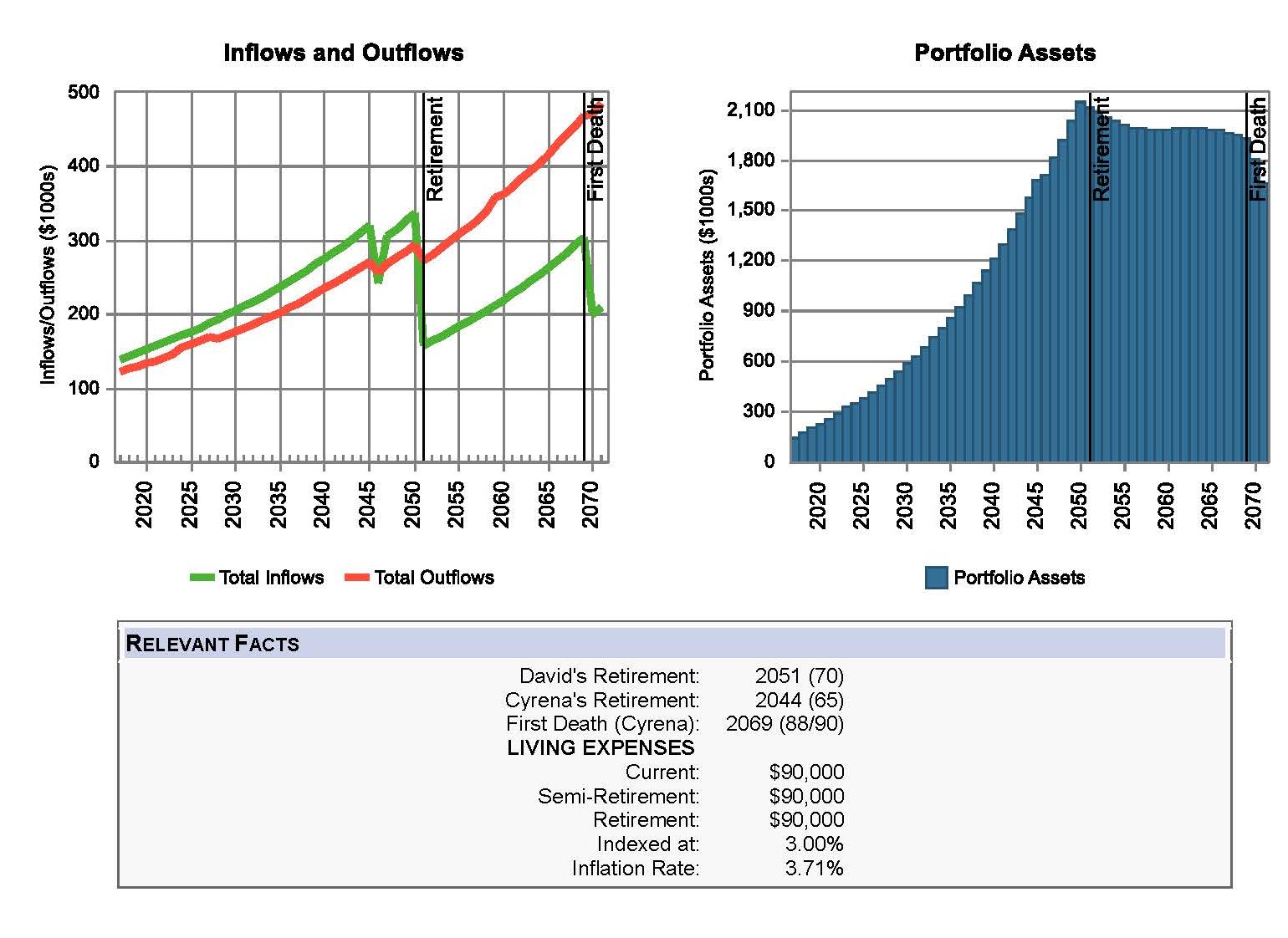

Here some of my conservative assumptions:

- We need about $90,000 of expenses in today’s dollars. This includes giving, health insurance, and our usual needs.

- If you add in our mortgage, that’s about $102,000 in total expenses

- I work full-time until 65 ($140,000 income in today’s dollars)

- I work part-time until 70 ($70,000 income in today’s dollars)

- A 3% Inflation rate

- My wife doesn’t earn any income. If she does, great! That will speed up the process more

- I did not factor the value of my business into the eq If I do sell it at some point, that could also allow us to retire significantly earlier

- I am not including any rate of return on my non-qualified savings

- I am not including the tax deferral benefits of a 401k or a Roth IRA

- We pay the minimum on our mortgage and don’t pay it off early

- We don’t get any inheritance from my folks (which will likely be fairly significant)

Here’s what my charts show:

To look at more detailed data, check out the tables below:

Today, we have about $135,000 in invested assets. Given this scenario, we need about $2 million to have a very comfortable retirement at 70 years old. If you add in the equity I currently have in my business, we have a net worth closer to $635,000 not including our house. So, we’re really about 1/3 of the way there already.

Of course, to retire earlier, we’ll need more and more assets. For example, we’d likely need $3,000,000 in assets to fully retire close to 63 to maintain our lifestyle.

I feel really great in knowing that given very conservative assumptions that retirement is still possible!

I also feel confident that a number of factors will make retirement even more likely at 55 or 60. It’s far enough away that I know we’re not close to it yet.

However, as we inch closer every year, I am going to be paying closer and closer attention to these numbers.

Final Thoughts

My friends, I’m not saying that retiring early is for everyone. As a matter of fact, I’ve shown that it isn’t for me.

The point of this blog post is to give you encouragement. There’s so much to your financial situation. However, no matter where you are at, there are solutions to move you forward. By having the right mindset and by crunching the numbers, you will know when you can retire.

Maybe that isn’t today. Maybe that isn’t tomorrow or five years or even twenty years away. That’s perfectly okay!

Just look at me. My family and I have big plans and big dreams and we’re willing to delay retirement to live for today. To give more. To enjoy life more and to live within our means.

However, we are still saving each and every day as we work towards our retirement goals.

Regardless of whether you are 25, 35, 45, 55, or 65, I want to encourage you that you have it within you to get to the next level. You have an amazing abundance of god-given talent and the ability to earn and save money. By digging deep and moving forward every day to your goals, I know you can achieve a liberated lifestyle.

What lessons have you learned from this case study? What are you going to do to move yourself closer to retirement?

Let me know what you think. Send me a comment at dave@daviddenniston.com or give me a ring at 952-831-8243.

Advisory services through Capital Advisory Group Advisory Services LLC and securities through United Planners Financial Services of America, a Limited Partnership. Member FINRA and SIPC. The Capital Advisory Group Advisory Services, LLC (CAG) and United Planners Financial Services are not affiliated.

The views expressed are those of the presenter and may not reflect the views of United Planners Financial Services. Material discussed is meant to provide general information and it is not to be construed as specific investment, tax, or legal advice. Individual needs vary & require consideration of your unique objectives & financial situation.